How to Avoid Lifestyle Inflation in Malaysia

Introduction

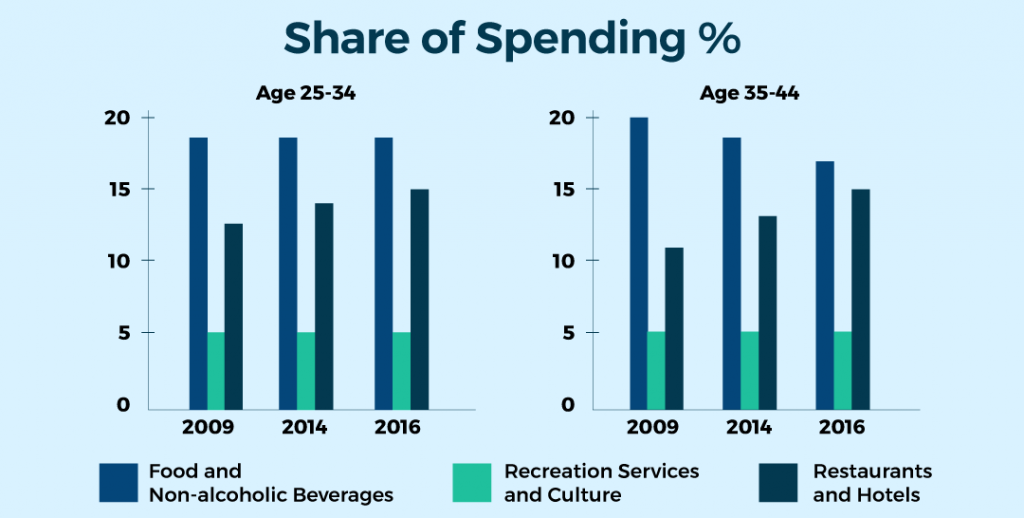

Are you earning more but still struggling to save? You might be a victim of lifestyle inflation in Malaysia. Many Malaysians increase their spending as their income rises, leaving little for savings or investments. This guide will show you practical ways to curb lifestyle inflation and take control of your finances.

What is Lifestyle Inflation?

Lifestyle inflation in Malaysia happens when your spending grows as your income grows. Instead of saving or investing extra income, many Malaysians upgrade their lifestyle—bigger rent, dining out more, buying expensive gadgets, or luxury cars.

Question: Have you ever noticed your expenses rising as soon as you get a raise? That’s lifestyle inflation at work.

Malaysians and the 50/30/20 Rule: A Practical Guide

Signs You’re Experiencing Lifestyle Inflation

- Increasing monthly spending despite higher income

- No significant growth in savings or investments

- Upgrading to luxury items immediately after a raise

- Frequent dining out or expensive travel without planning

Why Lifestyle Inflation is Risky in Malaysia

- Limits your ability to save for emergencies

- Slows wealth accumulation through investments

- Can lead to debt if you over-leverage to maintain a lifestyle

- Reduces financial freedom in the long term

How to Avoid Lifestyle Inflation in Malaysia

1. Track Your Spending

Use apps like Money Manager, BukuKas, or Spendee to monitor your expenses. Seeing where your money goes helps curb unnecessary upgrades.

2. Increase Savings First

Whenever you get a raise, automatically increase your savings and investment contributions before upgrading lifestyle.

3. Set Clear Financial Goals

Define goals like:

- Building an emergency fund of 3–6 months’ expenses

- Saving for property or retirement

- Investing in ASB, EPF top-ups, or stock market

4. Differentiate Needs vs Wants

Ask yourself if new purchases are essential or a result of lifestyle inflation. Needs come first; wants can wait.

5. Live Below Your Means

Even after salary increases, maintain modest living. Rent, groceries, and utilities don’t need to rise with income.

6. Automate Savings & Investments

Automating EPF top-ups, ASB contributions, or other investments ensures extra income is saved, not spent.

Examples of Avoiding Lifestyle Inflation in Malaysia

- Case 1: A fresh graduate gets a 20% salary increase but keeps rent the same and increases monthly savings.

- Case 2: A young professional upgrades tech gadgets only after setting aside 30% for investments.

Tools & Tips to Stay on Track

- Budgeting apps like YNAB or Spendee

- Maintain a fixed savings plan

- Set limits on discretionary spending

- Review expenses monthly to spot lifestyle creep

FAQs About Lifestyle Inflation in Malaysia

Q1: Is lifestyle inflation always bad?

Not necessarily. Moderate upgrades that don’t compromise savings or financial goals can be fine.

Q2: How can Malaysians with high living costs avoid lifestyle inflation?

Prioritize savings, automate investments, and find affordable alternatives for wants like dining, entertainment, and gadgets.

Conclusion

Avoiding lifestyle inflation in Malaysia is key to growing wealth, building savings, and achieving financial freedom. By tracking spending, automating savings, and living below your means, you can enjoy life while preparing for the future. Start small, stay disciplined, and watch your financial goals become reality!

Post Comment